Creating a retirement plan from a property portfolio

Every day there are people retiring from work and looking forward to a relaxed future full of travel and days out. Some of them have been landlords with a single, or multiple, private rented properties who are capitalising on the sale of their asset or simply years of accumulated rental income.

Shrewd investors know that alongside your pension and tax-free saving in ISAs, property is a sound place to invest your money for future growth.

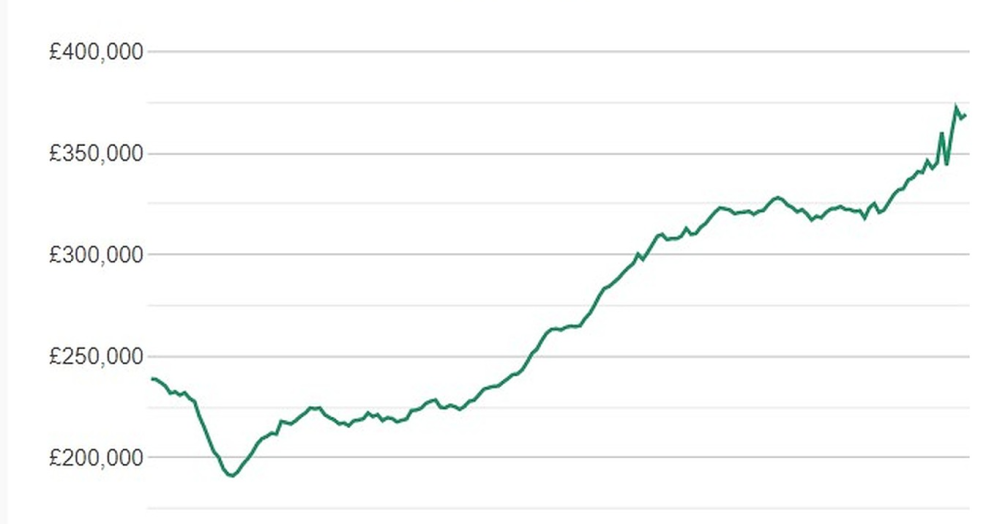

Owning property has been a reliable investment for decades. Despite fluctuations in the market when property prices dip and rise, if you take prices over a long period there is a continual rise. In the south east, the average house price has risen by 141k over the 10 years between Summer 2011 and Summer 2021 according to this chart (source: propertydata.co.uk).

In the current climate we face a shortage of property for sale and for rent. Every day at Capital Estate Agents we register potential tenants who have sold their property and are looking for a home to rent because they can’t find another property that they want to buy. Consequently, rents have increased by 3% in the South East in 2021 (per Homelet.co.uk). Very popular areas such as Bromley, Sevenoaks and Tunbridge Wells have seen higher percentage growth. If you can keep some of your investment properties during retirement then the rental income supplements your monthly pension income nicely.

Owning a rental property is not without its costs and risks. There are costs at the outset to buy a ‘buy-to-let’, including stamp duty and solicitors fees. There are maintenance and repairs to be managed and if you choose to appoint a letting agent to do this on your behalf, (which we would highly recommend) the cost of monthly management fees. The opportunity cost of putting your investment money into a property needs to be considered too as it means that you can’t put those funds into diverse funds which would spread your investment risk. On the basis of the potential return, combining rental income and capital growth, we’re sure you will agree that investing in property is a valuable way to grow your retirement pot.

Our experienced team at Capital Estate Agents are always happy to provide free and impartial advice on investing in buy-to-let properties. We would also recommend speaking to a financial adviser. Call Capital on 0208 313 0010 or email our team: info@capitalestateagents.com